The FAAA has welcomed the long awaited cessation of Dixon Advisory’s (Dixons) AFCA membership,

which ceased on 30 June 2024 after strong advocacy from the FAAA. This means there is now certainty

about the number of complaints about Dixons that AFCA will be investigating.

However the FAAA continues to express very deep concerns regarding the funding model for the

Compensation Scheme of Last Resort (CSLR), including the significant increase in exposure for the

financial advice profession.

“Now that Dixons’ AFCA membership has finally ceased – after two false deadlines, and almost 2.5 years

after being put into administration – we can see the full potential impact of this matter on our profession

and the costs we may need to pay for it, via the CSLR,” says Sarah Abood, CEO of the FAAA.

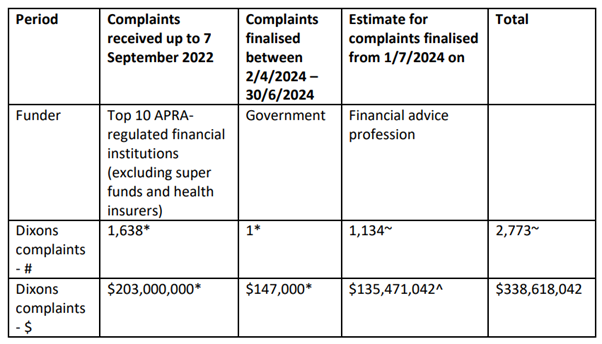

“Unsurprisingly, a number of additional complaints were made by Dixons clients in the final weeks of

AFCA membership, and the total number of cases registered with AFCA now stands at 2,773.

“While this is less than the administrator’s estimate of 4,606 investors whose losses in the US Masters

Residential Property Fund (URF) made them potential creditors, this is still a huge number of complaints

that will likely take years to process.

“These figures serve to highlight once again many serious flaws in the funding model for the CSLR, a

model which is both extremely unusual and extremely unfair – and in our view, fundamentally

unsustainable,” Ms Abood says.

Dixon Advisory – who pays, and how much?

*Estimated by CSLR actuary

~information provided by AFCA

^Complaint numbers from AFCA times average claim cost from the CSLR actuary of $119,463

($107,000 plus AFCA fee of $12,463)

“Estimates suggest financial advisers could be forced to pick up as much as $135 million of claims

related to Dixon Advisory, whilst the parent company (E & P Financial Group) has settled its class action

for around 4 cents in the dollar, while continuing to operate and advise many of the affected

clients. This highlights a deep flaw in the CSLR funding model that must be fixed. The Dixons scandal is

on such a massive scale that it warrants a public inquiry into the circumstances that led to this failure

and recommendations to ensure this cannot happen again.”

The FAAA has identified a number of actions it believes need to be urgently taken in order to fix the

CSLR funding flaws:

- The CSLR funding model must be prospective, not retrospective. Advisers should not be paying

for matters that occurred well before the scheme came into being. - The government needs to pay the first full year of operation of the scheme as was originally

promised, rather than just 3 months. - The government should re-instate the original sector cap (a maximum of $10 million that could

be levied per sector), rather than the $20 million that currently applies. - Our sector should be indemnified against future CSLR claims, where a matter has been reported

to ASIC and ASIC has chosen not to act, or has substantially delayed action. - The government must act to ensure that large vertically integrated groups cannot avoid paying

fair compensation to consumers by putting a subsidiary into administration. - The government must ensure that all other avenues for client compensation have been

exhausted before financial advisers are charged. - A party must be appointed to defend complaints against entities no longer in existence. At

present no-one is speaking for the advice provided to the consumer or defending these claims.

“We consider these actions to be urgent in order to secure a sustainable and fair funding base for the CSLR, so that consumers can continue to receive fair compensation if they have suffered a loss due to poor advice,” Ms Abood says